You spend weeks, sometimes months, deep in fieldwork. You’re tracing transactions, talking to stakeholders, and documenting every last detail. You finally wrap up the audit, pull your findings together, and send off the report, feeling pretty good about it. And then… crickets.

The report lands on a manager’s desk and becomes a permanent fixture. The recommendations you carefully put together are acknowledged with a nod and then forgotten. Nothing changes. All that effort feels like it was for nothing. It’s a story most internal auditors know.

But here’s the thing: the problem usually isn’t your audit work. It’s how you communicate it. The point of an audit report isn’t just to dump facts on a desk. It’s to persuade, to spark action, and to turn your hard-earned insights into real improvements for the business.

This article is your guide to breaking that cycle. We’re going to walk through a practical framework, the 5 Cs, that will help you move from simply pointing out errors to highlighting real business impact. It’s the key to writing reports that don’t just get filed away, but actually get read and acted upon by the people who matter.

What is impactful internal audit report writing?

Impactful internal audit report writing is really about translation. It’s the skill of taking complex, technical findings and turning them into a clear, concise, and persuasive story about business risk and strategic goals. It’s less about being a watchdog and more about being a trusted advisor.

The Institute of Internal Auditors (IIA) sets a high standard. According to their Standard 2420, every communication you release needs to be “accurate, objective, clear, concise, constructive, complete, and timely.” That’s a lot to live up to, but it all boils down to one thing: your report needs to be useful.

This is a far cry from the ineffective reports we’ve all seen (and maybe even written). You know the type:

- They’re so long and dense they could prop open a door, filled with jargon that only another auditor would appreciate.

- They get stuck on minor compliance details without connecting them to the bigger picture. They completely fail the “so what?” test.

- They’re written in a passive, academic tone that drains all the urgency from the issue.

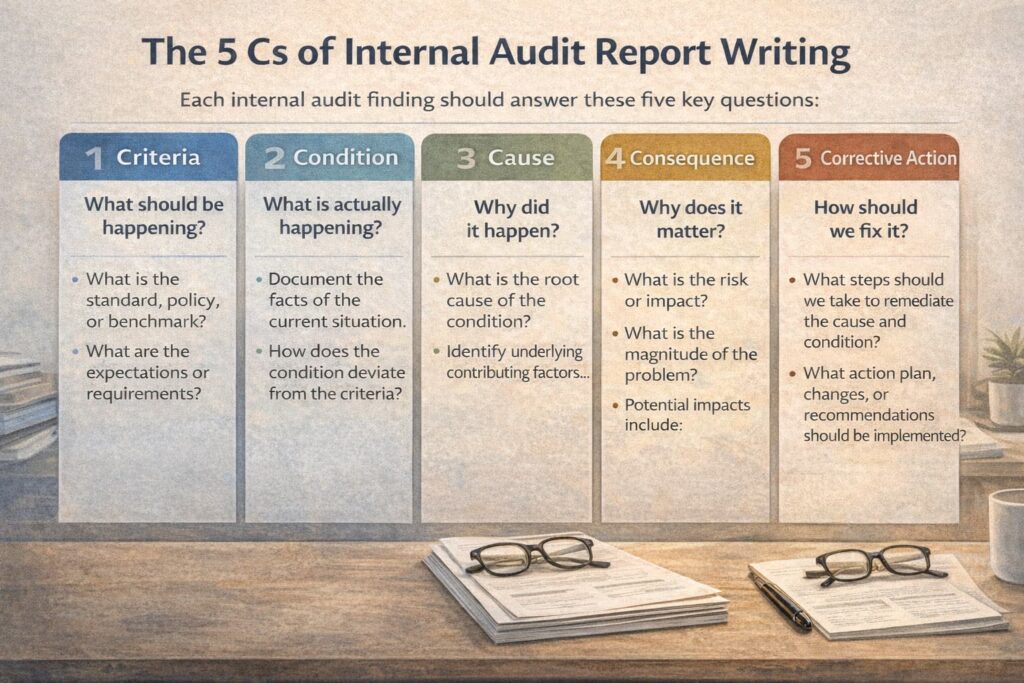

A great report tells a story about risk. It gives the board and senior management peace of mind where controls are working, and it builds an undeniable case for change where they aren’t. To do that, every observation needs a solid foundation. That’s where the “5 Cs” come in: Criteria, Condition, Cause, Consequence, and Corrective Action Plan. These are the essential building blocks for every impactful finding you’ll ever write.

Master internal auditing with confidence—enroll in the Internal Audit Masterclass today and elevate your professional edge!

The foundation of internal audit report writing

Structuring every single one of your findings using the 5 Cs forces you to build a complete, logical, and defensible point from start to finish. This framework, sometimes called the five attributes approach, is your best tool for making sure you always answer that critical “so what?” question that executives are asking.

1. Criteria (What should be)

First up is the criteria. This is the benchmark, the standard, the rulebook. It’s the policy, regulation, or best practice you’re measuring everything against. Simply put, it’s “what should exist.”

It’s vital to be specific and authoritative here. Don’t just say “according to best practices.” Cite the exact source. Whether it’s “Company policy 4.1.2 on data handling,” “Section 404 of the Sarbanes-Oxley Act,” or specific industry best practices, a clear criterion sets a firm, non-negotiable baseline for your finding.

Example: “The company’s vendor management policy requires a background check for all vendors with access to sensitive data.”

2. Condition (What is)

The condition is the reality on the ground. It’s the straightforward, factual statement of what you actually found. If the criteria is “what should be,” the condition is “what is.” It’s the gap between the two.

Your job here is to be objective and precise. This isn’t the place for opinions or vague statements. Use data, numbers, and hard evidence to paint a clear picture of the situation. The more specific you are, the harder your point is to ignore.

Example: “We found that 3 out of 10 new vendors with access to sensitive data in Q3 were onboarded without a documented background check.”

3. Cause (Why it happened)

Now we get to the interesting part: the “why.” The cause is your root cause analysis. It’s about digging deeper than the surface-level symptom (the condition) to figure out the underlying reason for the breakdown.

As audit expert James Roth suggests, you need to channel your inner toddler and repeatedly ask “why?”. Was the checklist flawed and the training insufficient? Was the system broken? Blaming “human error” is a cop-out. A good auditor finds the systemic reason the error was allowed to happen.

Example: “The onboarding checklist used by the procurement team does not include a mandatory step for verifying background checks before granting system access.”

See the difference? The root cause isn’t just a simple mistake; it’s a broken process.

4. Consequence (The “so what?” factor)

This is the big one. The consequence is the most important part of your finding and the one that will determine whether you get management’s attention. This is where you explicitly state the risk and the negative impact of the condition. It’s the “so what?” that turns a minor observation into a problem that needs to be fixed now.

You have to frame the consequence in terms your audience cares about: financial loss, reputational damage, legal penalties, or operational slowdowns. A great way to test if your consequence is strong enough is to use Mike Jacka’s “4 U’s framework”: Is the problem Unworkable, Unavoidable, Urgent, or Underserved? If you can’t articulate a compelling consequence, the business has no real reason to act.

Example: “This control failure exposes the company to a significant risk of data breach and potential regulatory fines under current data protection laws, directly answering the ‘so what?’ question.”

5. Corrective action plan (The recommended fix)

Finally, you need to outline the fix. But a simple recommendation isn’t enough. As the IIA Standards note, a report with only recommendations is only half-done. The goal is to collaborate with management before the report is finalized to get their buy-in on an agreed-upon corrective action plan. This turns the report from a critique into a constructive roadmap.

It’s helpful to think about two types of fixes:

- Condition-based recommendations: This is the quick fix for the immediate problem (e.g., “Immediately conduct background checks on the three vendors who were missed”).

- Cause-based recommendations: This is the long-term solution that tackles the root cause to make sure the problem never happens again (e.g., “Update the onboarding system to prevent vendor activation until the background check is confirmed”).

Example: “Management will update the procurement onboarding checklist to include a mandatory, non-skippable step for uploading proof of a completed background check before vendor accounts can be activated. The target completion date is Q4.”

Create an ATS-friendly resume with our Resume Builder.

Structuring your report effectively

Even if you’ve crafted perfect 5 C observations, they can still get lost if the report itself is a mess. A well-organized report is like a good tour guide; it leads busy executives straight to the information they need without any frustrating detours.

Start with a powerful executive summary

The reality is, many executives will only read the executive summary. This is your one-page shot to make an impact. It needs to be a concise overview that hits the key points: the audit’s objective and scope, your overall conclusion, and, most importantly, the most critical findings and their business impact.

Provide context in the introduction and background

After the summary, set the stage. Briefly state the audit’s purpose (objective) and what areas you covered (scope), including the specific time period you looked at. This is also where you should note any scope limitations, which are things you weren’t able to review that might have affected the outcome.

A little background can go a long way. Your report might be read by a board member who isn’t familiar with the day-to-day details of the process you audited. Give them just enough context to understand why the findings matter.

Organize detailed findings logically

When you get to the meat of the report, the detailed findings, organization is key. Don’t just list them chronologically or randomly.

- Group them: Cluster related findings under thematic headings like “Access Control Deficiencies” or “Vendor Management Risks.” This helps the reader see patterns and understand the scale of the issues.

- Prioritize them: Always put your highest-risk findings first. You want to grab their attention immediately with the issues that pose the biggest threat to the business.

- Title them clearly: Ditch generic labels like “Finding #1.” Use descriptive titles that summarize the problem, like “Lack of Formalized User Access Reviews.” This tells the reader exactly what the issue is before they even read the first sentence.

Tips for clear and persuasive writing

The final layer of a great report is the writing itself. The structure and content can be perfect, but if the language is clunky or unclear, your message will fall flat. Here are a few practical tips to make your writing sharp and persuasive.

Use a professional but direct tone

You can be professional without sounding like a robot. Write in a clear, direct style that’s easy to understand. Drop the overly formal language (“It was determined that…”) and avoid drowning your reader in technical jargon they won’t get.

One of the biggest improvements you can make is to use the active voice.

- Passive: “Quarterly reviews were not performed by the team.”

- Active: “The team did not perform quarterly reviews.”

The active voice is more direct, confident, and clearly assigns responsibility. And remember, your tone should always be constructive, not adversarial. You’re there to help fix problems, not to point fingers.

Show, don’t just tell, with examples and data

Vague statements are easy to dismiss. Hard data is difficult to argue with. Back up every point you make with specific numbers and real-world examples that illustrate the problem.

- Weak Example: “Vendor KYC was missing in some cases.”

- Strong Example: “Our review of 50 vendor payments found that 5 payments, totaling over $150,000, were processed to vendors with incomplete KYC documentation, exposing the company to regulatory penalties.”

The second example doesn’t just state a problem; it quantifies it and connects it to a tangible risk. That’s what gets attention.

Use visuals to break up text and clarify data

Nobody wants to read a 20-page wall of text. Use tables, charts, and simple graphs to present data and trends visually. A clean bar chart showing a spike in user access errors is far more powerful and easier to digest than a dense paragraph trying to explain the same thing. Visuals break up the monotony and make your key points stand out.

Turning reports into results

At the end of the day, the true measure of your audit report’s success isn’t its length or how many findings it has. It’s its ability to inform management and initiate necessary change.

You do that by shifting your focus from just listing problems to articulating business impact, the “so what?” factor. By building every finding on the solid foundation of the 5 C framework, structuring your report for a busy executive audience, and writing in a style that is clear and direct, you transform your report from a simple compliance document into a powerful tool for improvement.

An auditor’s real value isn’t just in finding the issues, but in communicating them so effectively that they actually get fixed. A well-written report is the most powerful tool you have to make that happen.

Call to Action: Writing compelling reports consistently is challenging. Our AI-powered platform helps audit teams draft clearer, more impactful observations in a fraction of the time. It guides you through the 5 Cs and suggests business-focused language, ensuring your insights get the attention they deserve. Learn more about how can elevate your audit reporting.

Master internal auditing with confidence—enroll in the Internal Audit Masterclass today and elevate your professional edge!

Also read: CA Articleship Transfer Rules & Interview Tips (Form 109 guide)

Frequently Asked Questions

Q1: What are the ‘5 Cs’ in internal audit report writing?

A1: The ‘5 Cs’ are a framework for structuring audit findings. They stand for Criteria (what should be), Condition (what is), Cause (why it happened), Consequence (the business impact), and Corrective Action Plan (the fix). This structure ensures every finding is complete and defensible.

Q2: How can I make my internal audit report writing more persuasive for executives?

A2: Focus on the “so what?” factor. Instead of just listing technical details, translate your findings into business risks that executives care about, like financial loss, reputational damage, or operational inefficiency. An executive summary with a high-level dashboard is also a great way to grab their attention.

Q3: What is the most common mistake to avoid in internal audit report writing?

A3: A common mistake is failing to explain the business impact (the ‘Consequence’). A report that only points out a rule was broken without explaining why it matters is likely to be ignored. Always connect your findings to a tangible risk.

Q4: Why is the ‘Consequence’ element so critical in internal audit report writing?

A4: The ‘Consequence’ is the part that answers the “so what?” question for management. It translates a technical control failure into a real business risk. Without a clear and compelling consequence, there’s no urgency for management to act on your recommendation.

Q5: Does the IIA provide specific standards for internal audit report writing?

A5: Yes, the Institute of Internal Auditors (IIA) sets the standards. Specifically, Standard 2420 on “Quality of Communications” states that audit reports must be accurate, objective, clear, concise, constructive, complete, and timely.