If you’re aiming for a top-tier audit role in banking or financial services, there’s one accounting standard you absolutely have to know inside and out: Ind AS 109, Financial Instruments. In technical interviews, this isn’t just another topic; it’s often the main event.

Plenty of candidates can recite the theory behind Ind AS 109. But when the interviewer asks them to explain its most complex part, the impairment model, in a practical way, things often get a little shaky. That knowledge gap is what separates a good candidate from a hired one, especially for those high-paying jobs in a Big 4 financial services audit team.

Ind AS 109, which aligns with IFRS 9, was introduced to fix the major weaknesses of the old “incurred loss” model. The flaws of that old system became painfully obvious during the 2008 global financial crisis. Banks were essentially waiting for defaults to happen before they recognized losses, a delayed approach to risk management.

This guide will break down the core concepts of Ind AS 109 that you need for your interview. We’re moving past generic theory and diving straight into the Expected Credit Loss (ECL) model, using a simple, real-world loan example to show you how it works.

What is the Expected Credit Loss (ECL) model?

The Expected Credit Loss (ECL) model is the forward-looking impairment framework at the core of Ind AS 109. Its main purpose is to make sure banks and other financial institutions recognize potential credit losses before they actually happen. It’s about anticipating future events rather than reacting to past ones.

To understand why this is such a big change, you need to know what it replaced. The old model under IAS 39 was called the “incurred loss” model. Under those rules, a bank could only book a loss when there was clear, objective evidence that a borrower had already run into trouble, like missing a payment. This was widely criticized for being a reactive, “too little, too late” approach. The provisions were often booked long after the economic conditions that caused them had developed.

The ECL model flips this entirely. It requires companies to look into the future from the moment a loan is issued. They have to consider a wide range of information, including past data, current conditions, and reasonable forecasts of future economic conditions, to estimate potential losses.

This shift from a reactive to a proactive model introduces a lot of judgment and complexity. How do you define a “significant increase in credit risk”? What economic forecasts are “reasonable”? These aren’t simple questions with easy answers. This is why audit firms are looking for candidates who can navigate these gray areas. It’s not just about knowing the accounting rules; it’s about understanding risk, data, and a bit of economic forecasting.

How the ECL model under Ind AS 109 works

Theory is one thing, but seeing it in practice makes all the difference. Let’s walk through a simple scenario.

Imagine a bank gives a 5-year loan of ₹1,00,000 to a small business on January 1, 2026. At that moment, the business has a strong credit rating, and the economy is looking healthy.

Day 1 (Stage 1)

Even though the loan is new and performing well, Ind AS 109 requires a provision from day one. The bank records a 12-month ECL, which reflects expected losses from defaults that could occur in the next year. It’s usually small but mandatory.

End of Year 1

Payments are on time and there’s no significant increase in credit risk (SICR). The loan stays in Stage 1, so the provision continues to be based on 12-month ECL.

End of Year 2 – Trigger for Stage 2

The borrower’s industry weakens and its credit rating is downgraded. Even without missed payments, risk has clearly increased. This SICR moves the loan to Stage 2, requiring a lifetime ECL provision for all possible defaults over the remaining loan term.

Check out our Ind AS Masterclass.

The three-stage impairment model

The ECL model is organized into three stages. These stages classify loans and other financial assets based on how their credit quality has changed since they were first created. Understanding what triggers a move from one stage to the next is a classic focus of interview questions.

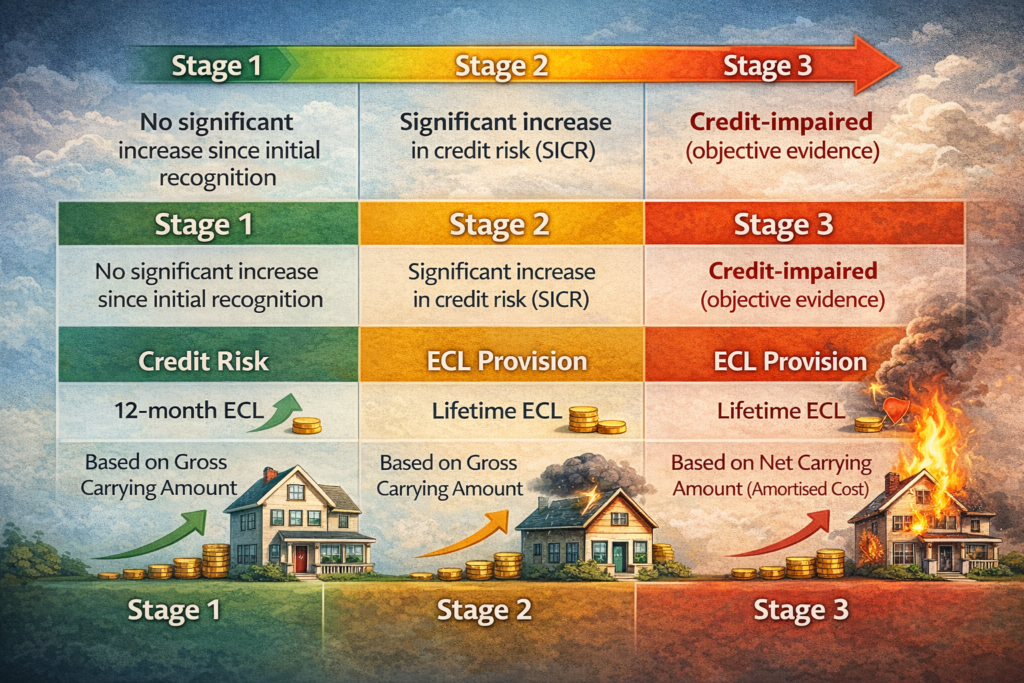

Stage 1 of Ind AS 109: Performing assets (12-month ECL)

This is the starting point for all new loans and financial assets. It’s also where assets that haven’t shown any significant increase in credit risk (SICR) since they were issued reside. These are considered healthy, low-risk assets.

The loss allowance, or provision, is measured as an amount equal to 12-month expected credit losses.

In simple terms, this is the baseline provision for every asset. It’s an acknowledgment that there’s always some risk of default, even for the best loans. It represents the portion of lifetime ECL that could result from default events possible within the next 12 months. A key detail for auditors is that for assets in Stage 1, interest revenue is calculated on the gross carrying amount, which is the total amount before deducting any loss allowance.

Stage 2 of Ind AS 109: Underperforming assets (lifetime ECL)

Stage 2 is for assets that have seen a “significant increase in credit risk” (SICR) since they were first recognized but aren’t officially credit-impaired yet. The borrower might still be making payments, but there are warning signs.

SICR is the main trigger here, and it’s a concept that requires a lot of judgment. It’s based on forward-looking information, not just a missed payment. Some common triggers include:

- A major internal or external credit rating downgrade.

- Negative changes in the business, financial, or economic environment.

- There’s also a rebuttable presumption that credit risk has increased significantly if payments become more than 30 days past due. This means it’s assumed to be SICR unless the company can prove otherwise.

Once an asset moves to Stage 2, the loss allowance is measured as an amount equal to lifetime expected credit losses.

Put simply, the bank now has to consider the risk of default over the asset’s entire remaining life. This leads to a much larger provision compared to Stage 1. However, just like in Stage 1, the interest revenue is still calculated on the gross carrying amount.

Stage 3 of Ind AS 109: Credit-impaired assets (lifetime ECL)

Stage 3 is for financial assets where there’s objective evidence of impairment. This is the stage where a loss event has actually happened or is clearly about to happen. The risk is no longer just a forecast; it’s a reality.

Examples of impairment events include the borrower being in significant financial trouble, a breach of contract (like a default on payments), or when payments are 90 or more days past due.

The loss allowance is also measured at Lifetime ECL, just like in Stage 2. The key difference is how you calculate interest revenue. For Stage 3 assets, interest is calculated on the net carrying amount (that’s the gross amount minus the loss allowance). This change reflects that the bank no longer realistically expects to recover the full amount.

Here’s a quick table to pull it all together:

| Feature | Stage 1 | Stage 2 | Stage 3 |

|---|---|---|---|

| Credit Risk | No significant increase since initial recognition | Significant increase in credit risk (SICR) | Credit-impaired (objective evidence) |

| ECL Provision | 12-month ECL | Lifetime ECL | Lifetime ECL |

| Interest Revenue | Based on Gross Carrying Amount | Based on Gross Carrying Amount | Based on Net Carrying Amount (Amortised Cost) |

Incurred loss vs. expected loss: A key question

One common interview question is: “Can you explain the difference between the incurred loss model and the expected loss model?” Answering this clearly shows you understand the core principle behind the standard.

The incurred loss model (the “rear-view mirror”)

This was the old way of doing things under IAS 39.

- Trigger: A loss was only recognized when there was objective evidence that a loss event had already occurred.

- Approach: It’s a reactive, backward-looking model that relied mostly on historical data of what had gone wrong in the past.

- Limitation: This always led to a delay in recognizing credit losses. It was the major weakness that the 2008 financial crisis exposed.

The expected credit loss (ECL) model (the “windshield”)

This is the new, forward-looking approach of Ind AS 109.

- Trigger: Recognition of losses is based on expectations of what might go wrong in the future. A provision is required from the very first day a loan is made.

- Approach: It’s a proactive, forward-looking model that combines historical data, current conditions, and future economic forecasts.

- Advantage: This leads to more timely recognition of credit losses, making financial statements a more accurate reflection of economic reality.

Preparing for the interview

Ind AS 109 is a complex standard, but it becomes manageable when broken down into its core components. For any financial services audit role, understanding the ECL model, its three stages, and the shift from an “incurred” to an “expected” loss approach is fundamental. Reading about these concepts is the first step, but articulating them clearly under interview pressure is what demonstrates true understanding. An interviewer will look for practical comprehension beyond textbook memorization.

Check out our Ind AS Masterclass.

Also read: 7 Salary Negotiation Tips for Chartered Accountants in 2026

Frequently Asked Questions

Q.1 What is the primary goal of the impairment model in Ind AS 109?

A: The primary goal is to shift from a reactive “incurred loss” approach to a proactive “expected credit loss” (ECL) model. This means recognizing and providing for potential credit losses before they actually occur by using forward-looking information, making financial statements more timely and reflective of true economic risk.

Q.2 How does an asset move between the three stages of Ind AS 109?

A: An asset starts in Stage 1. It moves to Stage 2 if there is a “significant increase in credit risk” (SICR) since its initial recognition. It then moves to Stage 3 when there is objective evidence of impairment, such as a default or payments being over 90 days past due.

Q.3 Why is understanding Ind AS 109 so important for a banking audit interview?

A: Ind AS 109 is central to how banks and financial institutions account for their primary assets (loans and investments). A candidate who can clearly explain its complex, judgment-based ECL model demonstrates a deep understanding of credit risk and financial reporting, which are critical skills for high-level financial services audit roles.

Q.4 What is the key difference in interest calculation for Stage 2 and Stage 3 assets under Ind AS 109?

A: Both Stage 2 and Stage 3 require a lifetime ECL provision. The key difference is in interest revenue recognition. For Stage 2 assets, interest is calculated on the gross carrying amount. For Stage 3 assets, interest is calculated on the net carrying amount (gross amount minus the loss allowance), reflecting the unlikelihood of collecting the full principal and interest.

Q.5 How did Ind AS 109 change the approach to loan loss provisioning compared to the old standard?

A: The old standard (IAS 39) used an “incurred loss” model, where losses were only recognized after a loss event happened. Ind AS 109 introduced the “expected credit loss” model, which requires recognizing a provision from day one of the loan and updating it based on forward-looking information, leading to earlier and more substantial loss recognition.

Q.6 What does ‘significant increase in credit risk’ (SICR) mean within the context of Ind AS 109?

A: SICR is the trigger for moving a financial asset from Stage 1 (12-month ECL) to Stage 2 (lifetime ECL). It’s a judgment-based assessment that considers forward-looking information like credit rating downgrades, adverse economic forecasts, or a borrower’s operational difficulties. There is also a rebuttable presumption of SICR if a payment is more than 30 days past due.