How to Conduct Forensic Audit: A Step-by-Step Guide in 2026

Introduction

Did you know? India saw a 46% rise in reported financial frauds in the past three years alone, according to data from the Reserve Bank of India. From fake invoicing and fund siphoning to insider trading and shell companies—financial crime is no longer the exception. It’s a growing business risk.

This is where forensic audit steps in.

Unlike regular audits that focus on compliance and accuracy, a forensic audit is more investigative in nature. It digs deep into transactions, records, and behaviors to find out if something shady has happened—like fraud, manipulation, or even criminal misconduct. It’s a mix of accounting, investigation, and legal knowledge used to detect fraud, collect evidence, and support legal action.

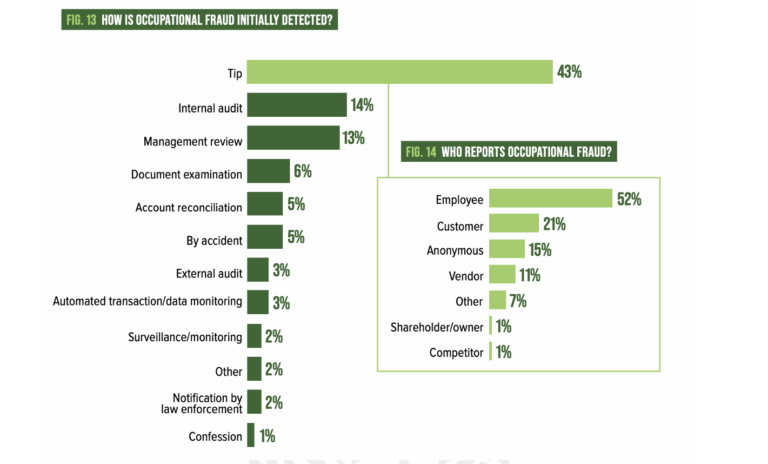

How is Fraud Initially Detected?

The Forensic Audit Process

A forensic audit is not a random investigation—it follows a structured and strategic process. Each step is designed to uncover the truth, gather solid evidence, and ensure that findings can stand up in a court of law.

Let’s break down the key steps involved in how to conduct forensic audit:

Step 1: Planning and Scoping the Audit

Before any investigation begins, the forensic auditor needs clarity of purpose.

They meet with management or the legal team to understand the issue:

“Is there suspected fraud? Missing funds? Data leaks?”They define the scope: what will be investigated, over what time period, and which departments are involved.

They also identify potential legal risks, ensure independence of the audit team, and prepare for confidentiality concerns, especially in high-stakes cases.

Step 2: Collecting Evidence

This is where forensic auditors go “undercover,” gathering both digital and physical proof.

Data sources may include: Accounting software logs, Emails, WhatsApp chats, phone records, Invoices, payment slips, and internal approvals, Security footage, access logs, biometric data

They follow the chain of custody—a formal process that documents how every piece of evidence was handled, to ensure it’s valid in legal proceedings.

Step 3: Analyzing the Data

Once evidence is in hand, auditors roll up their sleeves to analyze it.

They compare data over time to spot trends, anomalies, or sudden changes.

Use tools like ACL, IDEA, or Excel macros to sort large volumes of transactions.

Apply Benford’s Law (a statistical technique) to spot manipulated numbers.

Look for unusual transactions—like round-figure payments, weekend transfers, or multiple entries just below approval thresholds.

Step 4: Identifying Fraud Risks and Red Flags

Here’s where auditors start connecting the dots.

They identify transactions, departments, or individuals that show consistent patterns of abnormal behavior.

Cross-check internal records with external confirmations (e.g., call vendors, check GST filings).

Use visual tools like flowcharts or fraud matrices to map out how the fraud might have occurred.

Step 5: Verifying the Findings

You’ve found smoke—now look for fire.

Auditors validate suspicious transactions with additional documentation.

Conduct interviews or interrogations (in coordination with legal).

In high-stakes cases, forensic experts may collaborate with IT teams, cybersecurity professionals, or even law enforcement.

Step 6: Reporting the Findings

This is the final product—a formal report that outlines:

What happened

Who was involved

How it was done

How much was lost

What evidence supports the findings

Recommendations for next steps

The report must be clear, factual, and court-admissible. If it ends up in a legal case, the auditor may be called to defend the report in testimony.

Step 7: Legal Action and Ongoing Support

Once the report is submitted, companies decide how to proceed:

File an FIR or police complaint

Recover losses through civil litigation

Take disciplinary action against internal staff

Report the fraud to regulatory bodies (SEBI, RBI, SFIO, etc.)

In many cases, the forensic auditor remains involved to assist legal teams, appear in court as an expert witness, and help law enforcement with technical evidence interpretation.

Check how well your resume is crafted with our Resume Scorer tool.

Conclusion

A forensic audit does more than detect fraud. It builds trust, improves governance, and acts as a deterrent to future misconduct. From uncovering asset misappropriation to investigating insider trading, each audit plays a critical role in upholding financial integrity.

For finance professionals and CA aspirants, understanding forensic audits is not just a skill—it’s a career edge. As regulatory scrutiny tightens and demand for transparency grows, the need for trained forensic experts is rising across sectors: corporates, banks, startups, and even government bodies.

Whether you’re aiming to specialize in forensic accounting or just want to future-proof your finance career, mastering this process is a smart move. After all, in a world full of numbers—it’s the story behind the numbers that truly matters.

Join our Forensic Audit Masterclass and elevate your investigative skill

Looking for Opportunities?

Join the exclusive WhatsApp group to learn, network, and win together!